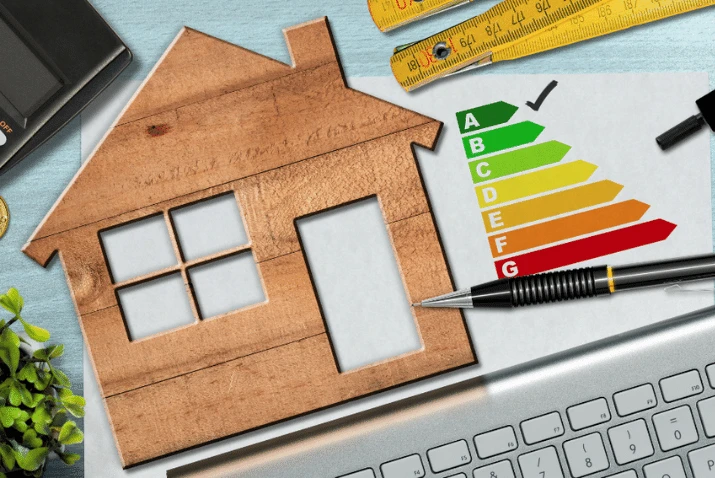

Since April 2018, landlords have been legally obliged to have a minimum EPC rating of ‘E’ in order to legally let a property or renew a tenancy – which was extended to existing tenancies in April 2020. Current proposals are for that to rise to a minimum ‘C’ rating for new tenancies in 2025 and all tenancies by 2028.

In addition, in their recent ‘Levelling Up’ white paper, the Government promised there will be a consultation later this year on introducing a legally binding Decent Homes Standard in the private rented sector for the first time. So, if your rented property is currently rated ‘D’ or ‘E’, it’s certainly time to look at what you can do to improve that to at least a ‘C’ sooner rather than later.

However while legislation could be seen as the ‘stick’ to force landlords to make properties more energy efficient, there’s now a ‘carrot’: green mortgages.

What are green mortgages?

Green mortgages are products that increasing numbers of lenders are making available to borrowers – both homeowners and buy-to-let investors – whose properties have an EPC rating of ‘A’ or ‘B’, and sometimes ‘C’. The products generally aim to have a combination of:

- A higher maximum loan to value

- A lower interest rate

- Lower fees.

The better your property’s energy rating, typically the more attractive terms you’ll be able to access, with the best deals reserved for ‘A’-rated homes.

Are green mortgages new?

Although you might not have been aware of them until now, green mortgages have actually been around since 2006, when Ecology Building Society started offering discounted rates to homeowners who were building or converting sustainable homes or making energy improvements. They were the only provider in the UK until Barclays launched its own Green Home Mortgage in 2018 for new homes that had EPC ratings of ‘A’ or ‘B’.

Last year there were two announcements that prompted more lenders to start incentivising borrowers to have energy efficient homes. In February, the Bank of England stated it was going to start carrying out ‘climate-related stress tests’ on UK banks and insurers and then the Government held a consultation on the proposal that lenders should have to disclose the energy efficiency of their mortgage portfolios.

Lenders currently offering green mortgages include Paragon Bank, Foundation Home Loans, Santander, Halifax and The Mortgage Works, and more are entering the market all the time. With the average home in the UK currently rated ‘D’, if this incentive encourages enough homeowners to make their homes greener, it could make a significant contribution to us reaching the Government’s target of ‘net zero’ by 2050.

How could a green mortgage benefit you as a landlord?

The most obvious benefit is that you could save money by paying a lower interest rate and less in up-front fees. Not only could your monthly payments be lower – giving you more rental profit in your pocket – but your total borrowing over time would be cheaper.

Secondly, if you could access a higher LTV mortgage and therefore buy with a lower deposit, that might enable you to grow your portfolio more quickly.

And thirdly, there are the positive impacts of having a more energy efficient property. It’s likely to protect and could even enhance the property’s capital value, and if the energy bills are lower, that makes the rent more affordable for tenants.

Depending on the product, you might be able to borrow via the mortgage to fund energy improvements, and the interest savings you make over time may even cover the cost of the works.

Will green mortgages become more popular?

Given the current proposals being discussed by Government around increasing the minimum EPC rating for landlords’ rental properties, it’s highly likely that green mortgages will increase in popularity in the coming years. As the Bank of England will begin to carry out ‘climate-related stress tests’ on UK banks and insurers, it’s expected that there will be more green mortgage options coming to the market too.

How can I find out more about green mortgages?

Of course, you can search online yourself to find green mortgage products, but you’re highly unlikely to find the best deals, given that around 75% of buy-to-let products are only available through brokers. You can also save a huge amount of time by speaking to a specialist who’s working in the market every day and has all the latest mortgage deals at their fingertips.

Our partners at Mortgage Scout will be happy to chat to you about what’s currently available on the green mortgage front and, if your property is not yet rated ‘C’ or above, they can let you know what help might be available for funding energy efficiency improvements.

For a more in-depth look at green mortgages and the whole buy to let mortgage market – the benefits of having a mortgage versus owning with cash, whether you should fix and for how long, and what the future holds for landlord financing – simply download our Mortgage eBook here.

And if you need any further advice regarding the energy efficiency of your rental or buy-to-let in general, simply contact your local branch and speak to one of the team.

There is no guarantee that it will be possible to arrange continuous letting of the property, nor that rental income will be sufficient to meet the cost of the mortgage.Your property may be repossessed if you do not keep up repayments on your mortgage.There may be a fee for mortgage advice. The actual amount you pay will depend upon your circumstances. The fee is up to 1%, but a typical fee is 0.3% of the amount borrowed.

MAB 15331

Please see article sources here.